Not all liquidity is created equal

By Colin Scanes, Market Surveillance Officer at Bitstamp

Introduction

When analysts look at the crypto market, they often highlight narrow spreads as one of the key indicators of good liquidity. But, in practice, the situation is much more complex than that. While having minimum spreads is good for some trading strategies, it effectively blocks many others. The key to a thriving global market is having trading venues with differently structured liquidity, so that traders are not limited in which strategies they can deploy profitably.

IN THIS ARTICLE, YOU WILL FIND:

- Why a model where fees are shared equally between makers and takers can actually be beneficial for both parties

- How it is possible to place highly competitive bids at Bitstamp that are very low compared to other exchanges

- How makers can post relatively large best bids that get hit rapidly but do not significantly impact price

- How takers at Bitstamp can sell at a lower price (or buy higher), but still receive more once fees are accounted for

The biggest determinant of an exchange’s microstructure is its fees. A number of the biggest crypto exchanges operate on a principle where most fees are covered by takers, while makers pay zero (or very little).

Bitstamp, on the other hand, shares the fees between makers and takers equally, which gives rise to the exchange’s specific microstructure and presents the market with unique options which it would otherwise be lacking.

Some historical background

Zero-fee and beyond that, rebate maker / taker pricing structures arose in the US equities market in the late 90s when the newly created Island ECN used rebates as a way to entice broker flow from Nasdaq onto their market. Naturally, any broker would prefer to get paid to trade on a venue by receiving a rebate than pay to trade somewhere else. All flow must go through a broker in the US equities market, so this created a conflict of interest for brokers who were obviously drawn by their economic interest of being paid to place orders with Island ECN – which was not always in the best execution interests of these brokers’ clients. If the best bid/ask price moved, they may miss the best price if the broker rested their order in the book rather than executed it immediately as a taker. Nevertheless, it was a success. Island ECN was taking a significant amount of the flow, so to remain competitive, the other US equities exchanges followed suit.

Zero-fee maker / taker model on crypto markets today

The practice in its zero-fee form was imported to the crypto markets by platforms like Coinbase and Kraken, but it took on a different market microstructural importance for these exchanges because of two major reasons. Firstly, there is no necessity to execute through a broker in the crypto markets, and secondly, the price of Bitcoin has a very small tick size (smallest value between successive prices) of down to 1 cent. When it comes to other asset classes, an instrument trading at $10,000 or above would trade with an exchange mandated smallest value move of $5, yet Bitcoin’s can be 500-times smaller.

Zero-market maker fees have created a distinct market microstructure in the order books where:

- The bid/ask spread has become 1 tick, meaning that the spread always gravitates towards 1 cent at Coinbase and 10 cents at Kraken (their respective tick sizes). When trading occurs, the spread widens momentarily, but will revert back to 1 tick.

- Market makers dominate price discovery, as most of the time it is impossible for a “natural buyer” who wants to save paying the spread to post a new best bid. With a 1-tick spread, a 1-tick better bid would mean a match with the best ask, forcing the buyer to pay a taker rate. The additional cost in taker fees for most buyers would be far greater than the consequence of the extra 1 tick paid in price.

- The result is a build-up of the order book queue at the best bid, meaning natural bidders have two things working against them: They can’t make a new best bid and they can’t be at the front of the queue, so they are forced to be stuck back in the queue, behind market makers, waiting for someone to hit both the market makers’ bids and then theirs.

Thus, we get the fallacy that a tight 1-cent spread and a high quantity of orders at the best bid and ask is a sign of “better” market liquidity. Not so! And it comes at a cost.

For the natural buyers who see the narrow spread and high liquidity and consequently decide to become takers, it means a much higher fee to pay. The higher fee cost from being a taker rather than a “fee-paying maker” considerably outweighs the benefit of the 1-tick spread.

The taker of 1 BTC paying $50,000 at a fee of 10 bps pays a $50 fee to benefit from that 1 cent spread.

Should everyone just try to be a maker?

Buyers who are not zero-fee market makers want to save the spread and pay the lower maker fee. Saving the 1-tick spread itself is of small help so they focus on the fee. The maker fee may not be zero for these buyers, but it is lower than the taker fee. They cannot make a new best bid and be at the front of the queue for the next taker sell order, because if they place a buy order 1 tick higher than the best bid, it would match them in the book with the best ask. So, they join the best bid, but are now stuck in a competitive queue, which requires a very fast reaction when the market changes to have any hopes of getting to the front.

For their trades to get filled, relatively large taker sell order(s) are required to reach their position in the queue. If the market moves up, they are likely to be left behind at the old best bid or have to re-join the queue at the new best bid, once again behind the speedy zero-fee market makers who got there first.

Alternatively, they stay at the old best bid and possibly get filled, but only when their bid gets to the front of the queue, as it has become stale. The bids in front of them have disappeared because the more informed market makers realized the market is about to fall and revised their own bid prices down. Their stale bid got adversely selected and now the best bid is lower than what they just paid.

How does Bitstamp differ?

The chief difference is that Bitstamp maintains a fairer share between what the maker pays and what the taker pays.

Firstly, with no zero-fee makers on Bitstamp, a 1-tick spread will never be made by someone operating a market-making strategy. If you wanted to capture the spread by quickly buying and selling as a maker, even if the fee were as low as 1 bps and the price were $50,000, the cost would still be $5 times 2 trades. So, $10 is the no profit, breakeven spread on 1 BTC. Even using a size of 0.1 BTC the market maker would be operating from a breakeven spread of $1.

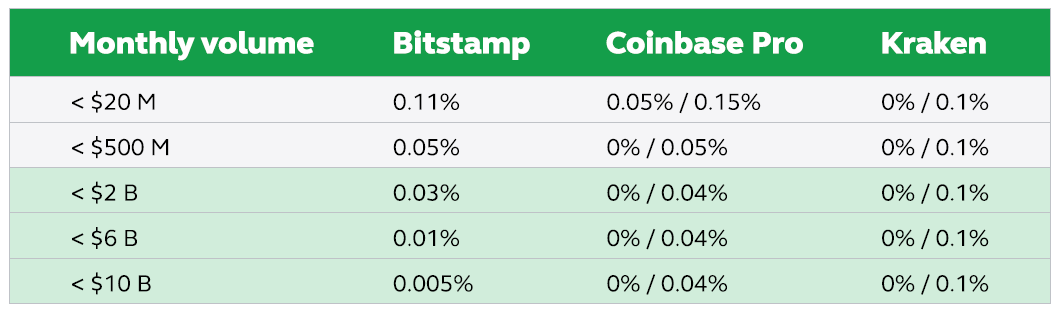

A market maker always risks being adversely selected, so if they are paying a fee to trade, they will want to trade at a spread that gives a decent profit, well beyond the $10. Hence the bid-ask spread on Bitstamp is much wider than on exchanges such as Coinbase and Kraken.

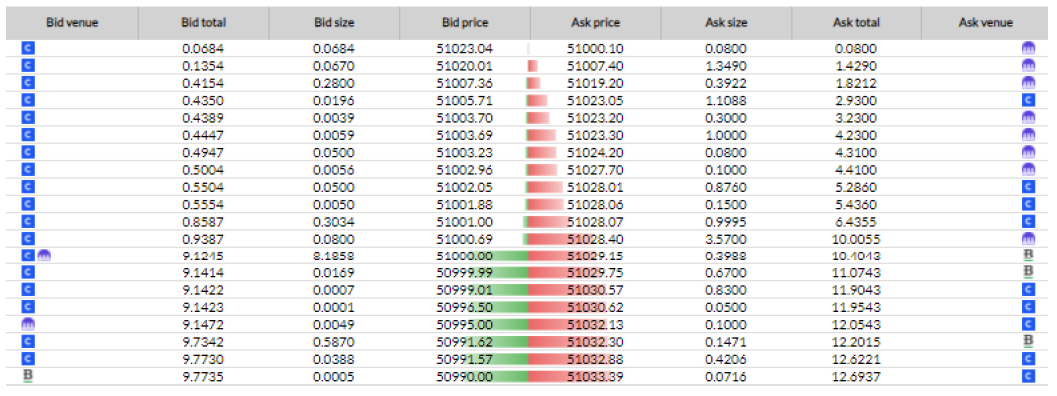

If those running a market-making strategy need to make a wider spread than 1 tick then this presents an opportunity. The buyer who is just looking to get long Bitcoin can place a bid at a better price than the current market-making bid and be at the front of the queue. The price of such a bid, although it is the best bid on Bitstamp, is likely to be much cheaper than the best bid that could be made or ask that could be taken at Coinbase or Kraken.

The hidden liquidity of takers

Compared to maker/taker fee models, Bitstamp's equal split between the two sides is actually more favorable to takers since they are the ones with the direct advantage of paying lower fees than on competing exchanges. Naturally, this leads to a relatively large number of players acting as takers, especially when it comes to the biggest high-frequency traders.

This large pool of takers significantly increases the liquidity of the exchange, however, it is not visible in the displayed volume you see in the order book. It is evident in the latent liquidity waiting to come into the market when a keenly new priced bid or ask appears.

If an exchange shares the cost of trading more equally between makers and takers, then the taker fee can be lower than in a structure where market makers are paying zero, leaving the taker to pay all of the exchange’s fees on a trade. This means large volume firms have a very attractive taker fee compared to the rate at zero-fee maker exchanges.

The reason latent liquidity can never be seen from an order-book snapshot is because it is only encouraged to reveal itself when a new best bid/ask comes in at a price favorable to the taker in terms of the price paid or received and fee the taker will pay.

What this results in is a market structure where the order books look relatively shallow around the best bid/ask, due to the lower incentive of makers to close the spread. However, this does not accurately reflect the venue’s liquidity, since there is a large amount of latent liquidity from takers just waiting for the right opportunity to arise. When this does happen, the makers’ orders get taken very quickly and it is very hard for the makers to exhaust the appetites of all the takers willing to accept their bid or ask.

When market data analysis firms look at liquidity and compare venues they always talk about narrow spreads, depth of order book and their calculation of slippage as being the signs of a liquid venue. They miss out on this whole area, largely because their data cannot express it. Bitstamp’s market structure leads to an accumulation of latent liquidity and it just requires traders making a new best bid (or, conversely, a new best ask) for it to reveal itself.

Who is Bitstamp’s microstructure good for?

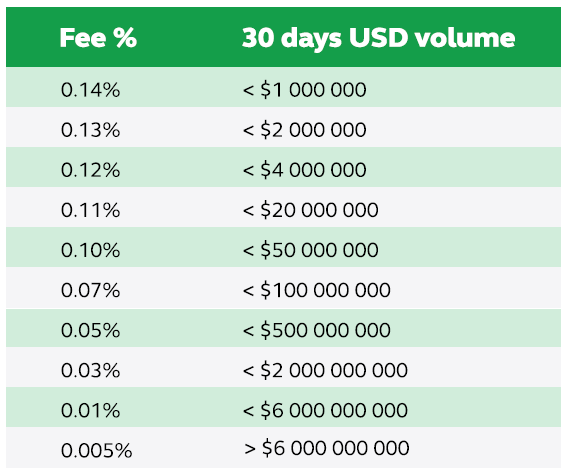

The short answer is anyone who posts new best bids and asks and becomes increasingly good for those with high monthly volume, since their rate falls with volume and Bitstamp’s fee schedule has more tiers for very high-volume traders. They have the opportunity, with a little patience, to buy at a cheaper all-in price (cost plus fee) and sell at a higher all-in price (income less fee) than they can at zero-fee maker exchanges.

BITSTAMP’S FEE SCHEDULE HAS ADDITIONAL HIGH-VOLUME TIERS

In short, Bitstamp’s attractiveness as a place to post new best bids comes from a combination of two things:

- The possibility to place a very low-priced bid relative to other exchanges in a way that it will still be the best bid on Bitstamp and have a cheaper all-in cost (bid price coupled with the fee) than if it were placed at the best bid on zero-fee maker exchanges.

- The latent liquidity of large takers who are relatively incentivised by the lower taker fee and so can take (sell) at a lower price but still receive more once the lower fees paid have been included.

Drawing the line

When the fees are spread more evenly between the two counterparties you get a better taker fee, which naturally leads to more incentivized takers.

In addition, on an exchange where fees are shared equally, makers can post relatively large new best bids and expect to be hit in short order while incurring no market impact, due to the absence of zero-fee makers closing the spread to one tick.

Of course all these points only come into play when looking at multiple exchanges at the same time. It is impossible to discuss the pros and cons of market microstructures in isolation, because one structure is not better than the other, rather, each provides opportunities the other does not.

In this way, exchanges with equally split fees, like Bitstamp, and exchanges with maker/taker models can act as complementary venues whose structures play off of each other to offer additional opportunities to high-volume traders.

About the author

As Market Surveillance Officer at Bitstamp, Colin Scanes is an expert on market microstructure across digital assets, equities, futures, options and FX. He has spent over 20 years working on the cutting edge of financial technology. Today, that’s brought him into crypto.